Celibacy tax

What is the relationship between the tax on celibacy and religious? Today’s in-depth study is dedicated to this issue.

During the Fascist regime, single status could be a luxury, a privileged and paid status.

In 1927, in fact, a specific tax was established for male individuals between 25 and 65 years of age who were not yet married; it did not apply to women.

The annual tax was instituted to induce as many male individuals as possible to marry and thus to generate children.

How was this tax to be reconciled with the religious, a large population of unmarried male individuals?

The latter were exempt from paying the tax but only if they took vows, one of which was chastity.

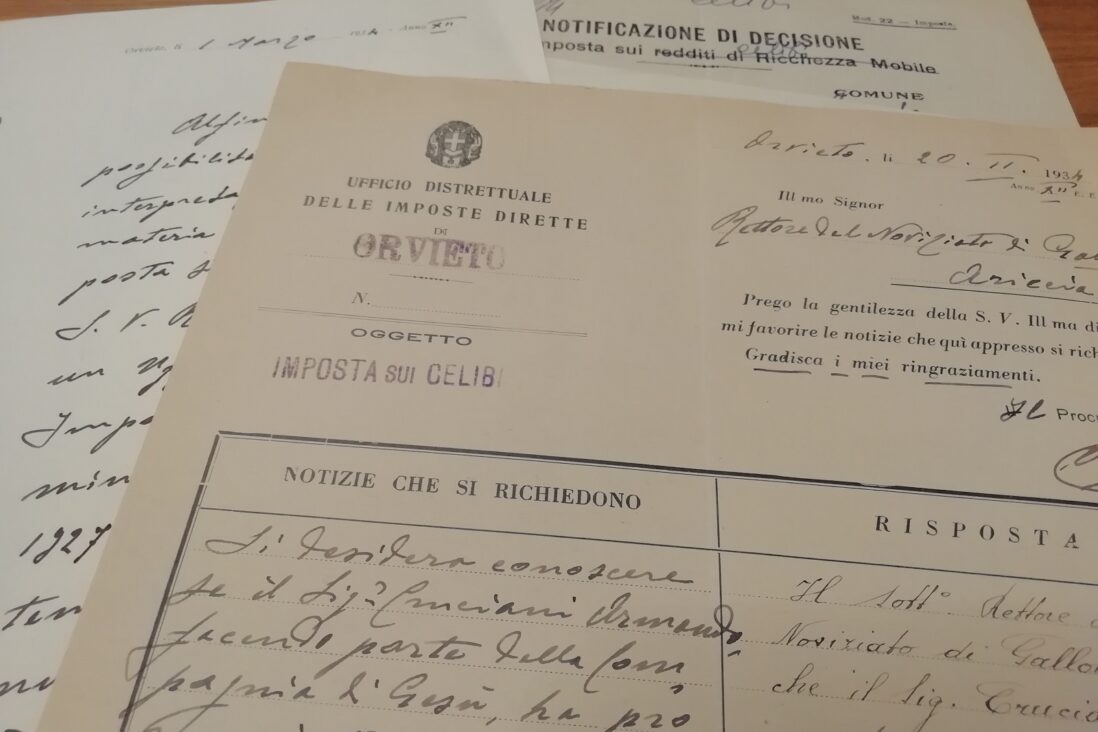

For this reason in 1934 the district office of direct taxes in Orvieto approached the Rector of the Galloro novitiate of the Roman Province.

The purpose of the missive was to ascertain whether or not the novice Armando Cruciani, a native of Orvieto, had taken the vow of chastity and to find out the date of his vows, in order to decide whether he should pay the celibate tax.

The letter is dated 20 February 1934, we do not have the Rector’s reply but it is easy to guess the answer from the rest of the correspondence and the novice’s stay in the novitiate.

Cruciani, nephew of a Jesuit of the Roman Province, officially entered the novitiate on 20 June 1934, but he had already been a postulant for several months, in fact the letter of parental consent for his entry into the novitiate dates back to 1932.

The novice therefore lives as a postulant and this is probably what the Rector reported to the office, perhaps believing that he would close the matter there. But this was not the case.

In the following letter of 1 March 1934, again sent by the direct tax office, the official replied to the Rector: “In order to eliminate any possibility of doubts and different interpretations of the law concerning exemption from the tax on celibates, I beg Your Reverend Excellency to find at any Direct Tax Office, Ministerial Circular n. 1714 of 1927, in order to be sufficiently informed that ‘the pronouncement of the vow of chastity is the only condition on which the enjoyment of the exemption depends for this category of citizens, regardless of the mission or function that each religious performs in the service of the Catholic Church. It is therefore indispensable to produce the declaration on whether or not the vow of chastity has been taken”.

The Rector probably still objects, perhaps referring to the condition of the novitiate and the length of time the novitiate requires before the pronouncement of the first you: two years. The office writes again on 6 March: “I am sorry to have to inform you that this office is not of the opinion of Your Reverend Reverend Reverence, since it is true that the pronouncement of religious vows is preceded by the novitiate, but it is also true that these vows may not take place, and for obvious reasons. Therefore, as long as the novitiate lasts, and the religious has not taken the vow of chastity, the religious himself is obliged to continue to pay the celibate tribute, strictly in accordance with the law’.

The letter specifies that after the vows, the novice could have asked for a refund of the tax and that the file was passed to the Albano Laziale office for territorial jurisdiction, since that is where Cruciani was living at the time.

The affair seems to have had a positive outcome a fewmonths later: a document from the Albano Laziale tax office dated 24 May 1934 attests to the novice’s status as a religious, exempting him from paying the tax.

Cruciani’s path would continue outside the Society of Jesus, but this affair has allowed us to investigate one of the aspects of religious life during the years of Fascism.

Maria Macchi